According to the most recent report from the federal government’s Bureau of Labor Statistics, the US economy added 142,000 jobs during August while the unemployment rate fell slightly to 4.2 percent. Since the highly disappointing July jobs report, media reports on the state of the job market have become far less positive. This report was described by CNN as “mixed news.”

Yet, the employment situation has not fundamentally changed from what has been common over the past year. Claims of solid, or even “blowout,” gains in employment throughout most of the past year have always been unconvincing if we look at the bigger picture. August’s “mixed” jobs report simply shows a continuation of the gradually weakening employment market that we have been seeing for months.

The lackluster nature of the employment market has been masked in these reports by a focus on a single data point within the report: the establishment survey’s total jobs number. Most reporting on August’s jobs numbers, for example, has ignored the fact that, according to the federal government’s household survey, the number of employed people in America has fallen over the past year. Moreover, the household survey suggests that much of the growth in “jobs” added by the establishment survey are due to made-up numbers created through the so-called “birth-death model” which simply assumes into existence hundreds of thousands of jobs created by hypothetical new businesses.

Let’s take a closer look.

Establishment Survey vs. Household Survey

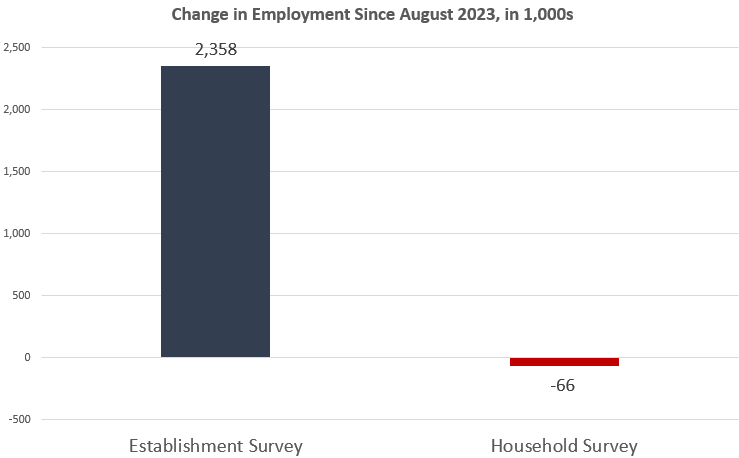

The establishment survey report shows that total jobs—a total that includes both part-time and full-time jobs—increased, month over month, in August by 142,000. The establishment survey measures only total jobs, however, and does not measure the number of employed persons. That means that even when job growth comes mostly from people working multiple part-time jobs, the establishment survey shows increases while the total number of employed persons does not. In fact, total employed persons can fall while total jobs increases. For instance, the total number of employed persons has fallen by 66,000 since August of 2023. This is in contrast to a gain of 2.3 million “jobs” in the establishment survey over the same period.

This is the first time the total number of employed workers has been negative, year over year, since the Covid recession of 2020. Whenever this measure turns negative, the US is either in recession or headed toward recession.

Moreover, if we look at the total increase in both measures of employment over the past three years, we find a gap has opened and persisted over more than two years. Indeed, as of the August report, the gap is at 4.2 million. In other words, since January 2021, the establishment survey has shown by nearly 16 million new jobs while the household survey has shown less than 12 million new employed persons. The graph of this gap shows how growth in employed persons has flatlined over the past fourteen months.

Which survey offers a better picture? Back in June, Bloomberg’s chief economist Anna Wong suggested the establishment survey is suspect, writing: “We believe the [household survey] currently offers a closer approximation of reality than [the establishment survey], as BLS’ model for estimating business births and deaths … is lagging the reality of surging establishment closures and falling business formation.”

(In August, that birth-death model added 100,000 jobs to the payrolls total.)

Assuming that the establishment survey is a realistic picture of the economy at all, then the current economy is producing many more jobs than actual workers.

A Recession in Full-Time Jobs

The economy is apparently adding far more part-time jobs than it is adding full-time jobs. In fact, the economy is rapidly shedding full-time jobs, and full-time job measures point to recession.

Over the past year, for example, total part-time jobs increased by 1.05 million. During the same period, full-time jobs fell by 1.02 million. In other words, net job creation during that period has been virtually all part-time. In the month of August alone, workers reported a gain of 527,000 part-time positions while full-time jobs fell by 438,000.

Year over year, total full-time employees fell 0.8 percent. Over the past five months, in fact, the year-over-year measure of full-time jobs has been in recession territory. Full-time jobs have now been down, year over year, in every month since February. Over the past fifty years, three months in a row of negative growth in full-time jobs has always been a recession signal and has occurred when the United States has been in recession, or about to enter a recession:

The full-time jobs indicator now reflects what we’ve seen in temporary jobs for months. For decades, whenever temporary help services are negative, year over year, for more than three months in a row, the US is headed toward recession. This measure has now been negative in the United States for the past twenty-two months. Temporary jobs in August were down by 5.2 percent.

Not surprisingly, other measures of employment point to a weakening economy. For example, in contrast to the headline unemployment rate, August’s U-6 measure of under-employment rose to 7.9 percent, a 35-month high, Job openings in the construction sector have experienced a historic collapse, dropping from 456,000 in February 248,000 in August.

If we take a larger look around, we find plenty of worrisome data in the leading indicators: The Philadelphia Fed’s manufacturing index is in recession territory. The same is true of the Richmond Fed’s manufacturing survey. The Conference Board’s Leading Indicators Index continues to point to recession. The yield curve points to recession. Net savings has now been negative for six quarters in a row. (That hasn’t happened since the Great Recession.) The economic growth we do see is being fueled by the biggest deficits since covid.

Having accepted that the economic and employment outlook is hardly positive, the debate is now over how much the Federal Reserve’s FOMC will cut the target policy interest rate at the FOMC’s September meeting. Ever since July’s jobs report, Fed policymakers have repeatedly signaled they plan to cut the federal funds rate soon. This, however, only points all the more to an impending recession. Recessions usually follow Fed rate cuts.

In spite of continued claims that the Fed will “engineer” a “soft landing,” the Fed has never succeeded in doing so. Ever.

The Fed’s lack of success in this regard isn’t because the Fed is unlucky or bad at timing its rate cuts. The problem stems from the fact that in situations like we are now in, the Fed only has two policy choices: it has to choose between rising price inflation or recession.

Experience shows that the Fed tends to prefer price inflation, and the Fed would rather force down interest rates and pursue easy-money policies all the time. The reason the Fed can’t do this is because easy-money policies cause place inflation, which often becomes a political problem for the regime.

So, when price inflation rises to politically unsustainable levels, the Fed must allow interest rates to rise and cut back on its easy-money policies. But, as Mises showed, an easy-money-addicted economy (such as the one we are now in) will enter the bust phase of the business cycle once there is less new money entering the economy. The only way the Fed can prevent a continued worsening in economic conditions right now is to turn back to easy money and again flood the economy with liquidity. However, the economy is now barely past a period of historically high levels of monetary inflation—i.e., “money printing.” A return to easy money will cause a new surge in rising prices. This is what happened in the 1970s during the Arthur Burns years. The Burns Fed tried to create a soft landing, but only succeeded in creating stagflation.

These are the options the Fed now faces. There is no soft landing coming.

Originally Posted at https://mises.org/

Stay Updated with news.freeptomaineradio.com’s Daily Newsletter

Stay informed! Subscribe to our daily newsletter to receive updates on our latest blog posts directly in your inbox. Don’t let important information get buried by big tech.

Current subscribers: