Futures Gain As Yen Resumes Slides, Oil Jumps

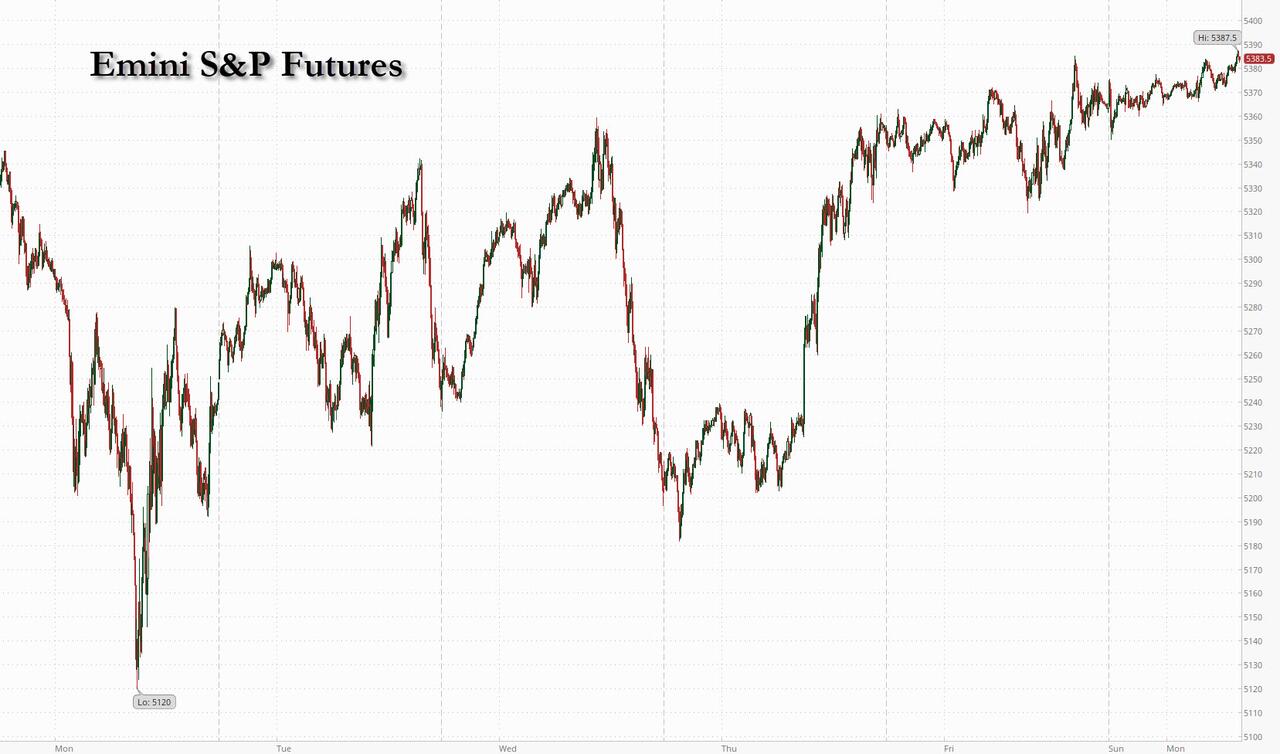

US equity futures are seeing a slight bid, tracking Asian and European markets higher, as the week starts off more muted than last week but with a preference towards Quality. As of 7:45am, S&P 500 and Nasdaq 100 contracts are about 0.3% higher as Mag7 names are mixed but net higher and Semis are bid, while Europe’s Stoxx 600 index erased most of a 0.5% advance. Bond yields are flat as is the USD while the yen continued dropping as more jawboning from an ex-BOJ member suggested that rate hikes in Japan are effectively over, giving a green light to restart carry trades . Commodities are stronger led by Energy, WTI is higher after adding 4.5% last week. Copper is higher after 5 consecutive weekly losses and 11 of last 12 weeks, -20% from highs. Today’s macro focus is the NY Fed’s 1-year inflation expectation (3.02% prior). This is a heavy macro data week with both growth and inflation measures and the market is waiting on that data to determine the next market narrative. Earnings are almost complete but DE, HD, and WMT will provide important updates on the Consumer.

{kind=link}

In premarket trading, Starbucks rose 2% after the WSJ reported that activist investor Starboard Value has taken a stake. Here are the other notable premarket movers:

- B. Riley Financial tumbles 25% after suspending its dividend as the boutique investment bank wrote down a portion of its stake in a US retail business.

- Hawaiian Electric falls 11% after pegging losses from estimated accrual of liabilities stemming from one of the worst wildfires in US history at $1.7 billion and issuing a going-concern warning.

- Humacyte sinks 12% as the FDA needs more time to review a biologic license application.

- JetBlue Airways slips 5% after announcing a $400 million convertible senior notes offering.

- KeyCorp (KEY) gains 14% after receiving a minority investment from Scotiabank.

- Monday.com (MNDY) rises 8% after posting a 2Q profit that topped estimates.

- Pacira BioSciences (PCRX) drops 4% after a court found its Exparel 495 patent not valid.

There was some relief for investors Monday from the volatility that ripped through markets in recent sessions, fueled by concerns the Fed is waiting too long to cut rates. The S&P 500 last week posted both its biggest one-day slump and best rebound since 2022.

“We all know that August tends to be a market in which we could see massive volatility simply because the liquidity does tend to be lower,” Sonja Marten, head of FX and monetary policy research at DZ Bank, said in an interview with Bloomberg TV. “This complete overreaction, panic move last week kind of goes to prove that.”

And while the VIX has retreated from its highest levels since the early days of the Covid-19 pandemic, there’s no certainty the relative calm will continue, with Wednesday’s US inflation data the key volatility event for the week. According to Citigroup, traders are positioning for the S&P 500 to move 1.2% in either direction when the consumer price index report is released.

Meanwhile, as bond markets have moved to account for a Fed that is “behind the curve,” the risk isn’t “priced into current equity multiples,” according to Morgan Stanley strategists. The team led by Michael Wilson said economic growth is the primary concern for investors, rather than inflation and rates. “Markets are looking for better growth or more policy support to get excited again,” the team wrote in a note. “We don’t see confirming evidence in either direction near term, leaving the index to trade in a tight range for now.”

Still, investors did take flight from stocks during last week’s wild swings. They reduced their equity allocations at the sharpest pace since the onset of the Covid pandemic, according to data from Deutsche Bank. Aggregate allocation to stocks is now in the 31st percentile and underweight, strategists including Parag Thatte wrote in a note dated Aug. 9. Just three weeks ago, exposure was at the top of the historical range in the 97th percentile.

Meanwhile, over the weekend we got a stark reminder that inflation still faces upside risks, after Fed Governor Michelle Bowman said she still sees upside risks for inflation and continued strength in the labor market, signaling she may not be ready to support an interest-rate decrease when US central bankers next meet in September. Money markets have fully priced a rate cut in September and about 100 basis points of easing for the year, according to swaps data compiled by Bloomberg. Separately, continued gains in oil in the next few weeks may throw a wrench in the Fed’s rate cutting plans.

“The problem is also that central banks have been emphasizing that they are acting very data-dependent these days,” DZ Bank’s Marten said. “Investors are trading from one data point to the next. That does also create additional volatility.”

Elsewhere, the European Central Bank is now seen as likely to cut its deposit rate once a quarter through the end of next year, a timetable that will see its easing cycle end sooner than previously anticipated. A Bloomberg survey of forecasters shows that benchmark hitting 2.25% in December 2025 following six consecutive quarter-point reductions.

European stocks erased gains as more sectors turn red, with traders preparing for a busy week on the data front. Real estate and health care lag peers, while energy and miners lead climbers. UK’s FTSE 100 outperforms regional peers with a 0.3% rise. In London, BT Group Plc rallied more than 7% after Bharti Global agreed to buy a stake of about 24.5% in the UK carrier. Here are some of the other biggest European movers on Monday:

- Hannover Re rises as much as 6.3%, the most since November 2020, after the German reinsurer reported net investment income that beat the average analyst estimate in the second quarter. Jefferies says the strength of mid-year renewals prices supports the outlook.

- Eutelsat shares rise as much as 4.6% Monday after the satellite operator said it’s exploring a sale of a majority stake in its satellite ground infrastructure to EQT.

- Orlen shares rose most since April 2 after Poland’s largest energy company reported preliminary earnings that beat analyst expectations.

- JDE Peet’s shares fall as much as 1.7% after the coffee company announced its interim CEO and chairman Luc Vandervelde will step down, just five months after the exit of its former chief executive. The loss of yet another CEO in a short space of time makes the company look “careless,” ING analysts say.

- JD Sports shares fall as much as 2.8% after the sporting goods retailer was downgraded to sell from hold at Deutsche Bank, which said the stock is trading at an “unwarranted” free cash flow yield premium to peers.

- Marshalls shares drop as much as 5.3% after the landscaping, building and roofing products supplier reported sharp double-digit drops in revenue and earnings in the first half. Peel Hunt said this was driven by challenging conditions for its Landscaping arm.

- Aryzta shares decline as much as 4.5% after the Swiss industrial baker reported first-half organic growth that Vontobel described as “weak.”

Earlier, Asian equities advanced for a second session as technology stocks in South Korea and Taiwan extended a rebound from last week’s rout. The MSCI Asia Ex-Japan Index climbed 0.4%, kicking off the week on a positive note after declining for four straight weeks. Technology stocks in the region, including Taiwan Semiconductor Manufacturing Co., Tencent Holdings Ltd., Hon Hai Precision Industry Co. and Samsung Electronics Co., were among the biggest contributors to the gains. Japan is closed for a holiday. Artificial intelligence-related stocks are regaining momentum after a brutal selloff last week that saw an unwinding of some of these crowded trades. Traders will shift their focus to key US data prints this week as they assess the possibility of a recession in the world’s largest economy.

In FX, the Bloomberg dollar spot index is steady. NZD and AUD are the strongest performers in G-10 FX, JPY and CHF underperform. Dollar-yen is at around 147.6: the yen dropped the most against the dollar among major peers after former board member Makoto Sakurai said the Bank of Japan won’t be able to raise the policy rate again this year, given the market turmoil that followed its recent hike and the low likelihood of the nation’s economy seeing a rapid recovery. That followed last week’s surge as traders slashed bearish bets in the wake of the Bank of Japan’s July 31 rate hike. The BOJ’s move prompted investors to dump carry trades, unleashing turmoil that ricocheted across global markets.

In rates, treasuries are slightly cheaper across the curve, although yields remain near to Friday’s closing levels and spreads remain steady. Treasury 10-year yields trade around 3.955%, cheaper by about 1bp on the day, with bunds lagging by ~1bp in the sector. Treasury spreads are broadly within 1bp of Friday’s close. Fed comments over the weekend included Governor Michelle Bowman, who said she sees upside inflation risk, signaling caution on rate cuts. In Asia, China 10-year yields rose as much as 5bps, as the central bank warned on potential risks arising from the relentless rally in the debt market.

In commodities, oil extended its first weekly gain since early July, with traders continuing to monitor Iran’s response to last month’s assassination of a Hamas leader in Tehran. WTI futures are higher by 1.1%, supporting energy names; Brent rises 0.6% near $80.15. Spot gold rises roughly $13 to trade near $2,444/oz, the highest in a week. Spot silver gains 1.4% near $28. Most base metals trade in the green.with traders focused on the week’s key US data. Bullion has gained more than 18% this year and remains in touching distance of last month’s all-time high. Along with rate-cut expectations, it’s also been supported by firm central bank buying and robust demand from Chinese consumers.

Looking today’s calendar, it is a quiet session for scheduled events: the US data slate includes July New York Fed 1-year inflation expectations (11am) and monthly budget statement (2pm).No Fed speakers scheduled for the session

Market Snapshot

- S&P 500 futures up 0.3% to 5,384

- STOXX Europe 600 up 0.3% to 500.51

- MXAP up 0.1% to 175.65

- MXAPJ up 0.4% to 555.47

- Nikkei up 0.6% to 35,025.00

- Topix up 0.9% to 2,483.30

- Hang Seng Index up 0.1% to 17,111.65

- Shanghai Composite down 0.1% to 2,858.21

- Sensex up 0.3% to 79,947.89

- Australia S&P/ASX 200 up 0.5% to 7,813.70

- Kospi up 1.2% to 2,618.30

- German 10Y yield little changed at 2.24%

- Euro little changed at $1.0919

- Brent Futures up 0.6% to $80.14/bbl

- Gold spot up 0.4% to $2,439.83

Top Overnight News

- Federal Reserve Governor Michelle Bowman said she still sees upside risks for inflation and continued strength in the labor market, signaling she may not be ready to support an interest-rate decrease when US central bankers next meet in September

- US VP Harris said she will work to raise the minimum wage and eliminate taxes on tips for service and hospitality workers, copying Trump policy promises

- US-China working group set to meet in China this week: NYT

- In Secret Talks, U.S. Offers Amnesty to Venezuela’s Maduro for Ceding Power: WSJ

- Oil steadied after its first weekly gain since early July, with the market still waiting for Iran’s response to last month’s assassination of a Hamas leader in Tehran

- The Bank of Japan won’t be able to raise the policy rate again this year, given the market turmoil that followed its recent hike and the low likelihood of the nation’s economy seeing a rapid recovery, according to a former board member

- Former Treasury Secretary Lawrence Summers urged the Securities and Exchange Commission and relevant exchanges to look into the historic surge in the most-watched gauge of US financial volatility on August 5

A more detailed look at global markets courtesy of Newsquawk

APAC stocks began the week mostly higher following last Friday’s gains on Wall St and light macro newsflow over the weekend, but with gains capped amid an indecisive mood in China and holiday closure in Japan for Mountain Day. ASX 200 advanced with the upside led by outperformance in Consumer Discretionary, Tech, Telecoms and Financials. Hang Seng and Shanghai Comp. were indecisive as lingering economic concerns offset the PBoC’s liquidity efforts.

Top Asian News

- PBoC’s low carbon financing scheme which provides financial institutions with low-cost loans targeting carbon emission cuts was extended to the end of 2027, according to the State Council.

- RBA Deputy Governor Hauser said economic forecasts are subject to huge uncertainty and assume inflation stickiness due to weaker supply and labour market tightness, while he added there is risk consumption could rise more strongly, in part due to an increase in wealth and it is uncertain how far and fast the savings rate might rise.

- Chinese brokers curb bond trading amid warnings of a rally, via Bloomberg; at least four brokerages have started fresh measures to cut back trading on government bonds since last week.

European equities, Stoxx 600 (+0.3%) have started the week on a mostly firmer footing, taking positive leads from a constructive APAC session. European sectors hold a strong positive bias. Insurance takes the top spot, propped up by post-earning strength in Hannover Re. Basic Resources and Energy are both higher, given the strength in underlying commodity prices. US Equity Futures (ES +0.2%, NQ +0.3%, RTY -0.1%) are mixed, with the ES and NQ very modestly firmer, benefiting from the generally positive risk tone.

Top European News

- BoE’s Mann said UK wage growth is still a concern for inflation and goods and services prices were set to rise again, while she added that wage pressures in the economy could take years to dissipate. Furthermore, Mann said she moved down from ten to seven on a scale of “hawkishness” since the start of the year as price pressures eased, according to FT.

- Fitch affirmed Netherlands at AAA: Outlook Stable, while it affirmed Finland at AA+; Outlook Revised to Negative.

FX

- DXY is trading relatively flat and within tight ranges of 103.12-24, in what has been a catalyst thin session thus far. This week’s focus is on US inflation data, followed by Retail Sales.

- EUR is choppy but within tight ranges and largely moving at the whim of the buck in the absence of any further catalysts. EUR/USD remains within Friday’s 1.0908-1.0931 parameter.

- GBP/USD experienced early upticks as EUR/GBP briefly dipped under 0.8550 (to 0.8544 low) in turn propping up GBP/USD which found resistance just shy of its 50 DMA (1.2784), with the pair’s current range between 1.2748-1.2782 range. Overnight, BoE’s Mann said UK wage growth is still a concern for inflation.

- JPY is the marked laggard with Japanese players away overnight on Mountain Day holiday. Traditional haven FX are hit despite the geopolitical uncertainty. Price action in the JPY has been gradual and contained to within Friday’s range between 146.26-147.81.

- Antipodeans outperform, benefitting from the overall risk tone and strength in the metals complex. NZD/USD is back above the 0.6000 level ahead of the RBNZ meeting where there are mixed views on whether the central bank will cut rates or not.

- PBoC set USD/CNY mid-point at 7.1458 vs exp. 7.1777 (prev. 7.1449)

Fixed Income

- USTs are subdued after hitting a high of 113-05 last Friday, leading to a slight pullback. Price action has been fairly rangebound, given the lack of pertinent newsflow, so attention remains firmly on US CPI mid-week. Currently trading around 112’25.

- Bunds are modestly softer with the broader bond complex inching lower since the uneventful APAC trade, with some potential follow-through from the upticks in oil and gas prices on yields.

- Gilts are slightly lower but still comfortably above the Aug 8 low of 99.20. The UK docket is quiet today. Overnight, BoE’s Mann said UK wage growth is still a concern for inflation and goods and services prices were set to rise again.

Commodities

- Crude is firmer intraday and inching higher amid geopolitical uncertainty over Iran and Lebanon’s response against Israel to the assassinations of the Hamas leader and Hezbollah commander, with the risk of the response sparking a region-wide war.

- Natural Gas is firmly in the green amid broader energy upside. Dutch TTF holds north of EUR 40/MWh and closer to EUR 41/MWh as the Ukrainian offensive within Russia widens, with Russian authorities suggesting the situation in the Belovsky border region in Kursk is very tense.

- Metals are firmer across the board with precious metals buoyed by geopolitical angst and base metals held up by the broader risk tone alongside some fears of sluggish global growth abating. Spot gold topped last week’s high to trade in a current USD 2,423.67-2,442.70/oz range at the time of writing.

- Iran’s President nominated Mohsen Paknezhad as Oil Minister and Abbas Aragchi as Foreign Minister.

- OPEC Monthly Oil Market Report to be published at 11:45BST / 06:45EDT

Geopolitics: Ukraine

- “IDF Radio: The final decision on the direct attack has not yet been made and is in the hands of the Iranian leader… The Iranian attack, if carried out, will be limited and will not lead to a wide regional war”, Via Ashaq News. “Israeli Army Radio: Iran is close to deciding to launch a direct attack from its territory towards Israel”

- Israel conducted an air strike which killed nearly 100 in a Gaza school refuge, according to civil defence officials cited by Reuters. It was also reported that Israel ordered a major evacuation in Gaza’s Khan Younis.

- Israeli media reported that at least 30 rockets were fired by Hezbollah towards Israel of which some were intercepted by air defences, while no casualties were reported from the rocket shelling on the city of Nahariya and its suburbs.

- Israeli intelligence believes Iran has decided to attack Israel directly and may do so within days, according to Axios’s Ravid. It was also reported that Israeli Defence Minister Gallant spoke to US counterpart Austin and told him Iranian military preparations suggest Iran is getting ready for a large-scale attack, while Israeli intelligence assessment indicated an Iran attack may precede ceasefire talks scheduled for Thursday. Furthermore, Israel’s military intelligence and air force raised the alert level amid the threat from Iran.

- US Defence Secretary Austin told Israeli counterpart Gallant he ordered the USS Abraham Lincoln carrier strike group to accelerate its transit to the Middle East, while he also ordered the USS Georgia guided missile submarine to the Central Command region.

- Iran’s Revolutionary Guards held a military drill in West Iran, according to IRNA.

- Hamas asked mediators to present a plan based on past talks instead of engaging in new negotiations, according to a statement.

- Several US and coalition personnel suffered minor injuries in an attack in Syria on Friday, according to a US official cited by Reuters.

Geopolitics: Other

- IAEA said its experts witnessed a strong dark smoke coming from the northern area of the Zaporizhzhia nuclear plant following multiple explosions but added that there was no safety impact reported.

- Ukrainian President Zelensky said Russia started a fire on the premises of the Zaporizhzhia nuclear plant in southern Ukraine but added that radiation indicators are normal. It was also reported that the Russian management of the Zaporizhzhia nuclear plant accused Ukraine of causing a fire near the cooling towers of the Zaporizhzhia nuclear plant by shelling the nearby city of Enerhodar although it noted that the fire had no impact on its plant and its safe use.

- Main fire at the Russian-controlled Zaporizhzhia power plant in Ukraine had been extinguished, while Russian and Ukrainian authorities said in separate statements that one of the cooling towers at the power plant was damaged, according to Reuters. Furthermore, Russian President Putin ordered tighter security at strategic facilities in Zaporizhzhia including the nuclear plant.

- Ukrainian President Zelensky said Russia conducted nearly 2,000 cross-border strikes on Ukraine’s Sumy region from the Kursk region this summer and such strikes deserve a fair response from Ukraine. Zelensky also commented that Russian forces used a North Korean missile in a strike on the Kyiv region which killed two people, while the Ukrainian military said it destroyed 53 attack drones launched by Russia during a strike over the weekend.

- Russia’s Kursk region governor ordered a faster evacuation of civilians in areas at risk of Ukraine’s attack and announced that thirteen people were injured from a downed Ukrainian missile in Russia’s Kursk city, while it was reported that Russia’s air defence systems destroyed 14 Ukraine-launched drones and four missiles over the Kursk region.

- Belarusian President Lukashenko said Belarus’s air forces were put on high alert after Ukraine violated Belarus’s air space and Belarus destroyed objects thought to be Ukrainian drones that had entered their air space.

- Philippine military said a Chinese air force aircraft executed a dangerous manoeuvre and dropped flares in the path of a Philippine air force aircraft in the South China Sea shoal. Furthermore, the Philippines presidential office said the action of the Chinese aircraft was unjustified, illegal and reckless, while President Marcos strongly condemned the air incident at Scarborough Shoal.

US Event Calendar

- 11:00: July NY Fed 1-Yr Inflation Expectat, prior 3.02%

- 14:00: July Monthly Budget Statement, est. -$242b, prior -$66b

Tyler Durden

Mon, 08/12/2024 – 08:13