After Victory, Trump Faces the Big Economic Problems

Ryan and Tho talk about what Donald Trump must do if he wants to actually fix our mounting economic problems of stagnation, debt, and inflation.

NewsWare‘s_Trade_Talk

- Business , Economics , News

- November 7, 2024

- 11 views

NewsWare’s Trade Talk: Thursday, November 7 | NewsWare‘s Trade Talk

S&P Futures are displaying gains this morning after yesterday impressive rally. The markets are awaiting a monetary policy decision from the FOMC today. On the earnings front APP, ELF, LYFT, MCK, QCOM, DDOG & RL are higher after announcements. After the bell today, ANET, ABNB, TTD, SQ, DKNG & RIVN are scheduled to release. Data on Jobless Claims & 3Q Productivity & Cost to be released before the opening bell. In Europe, stocks are higher, The FTSE is only showing a minor gain ahead of today’s BOE decision. Oil prices are showing some weakness this morning.

Woke Bloodbath: Leftist Movements Are Paying The Price For Their Arrogance

By Brandon Smith If you thought Kamala Harris was a sure win in 2024, then you haven’t been paying attention…

The post Woke Bloodbath: Leftist Movements Are Paying The Price For Their Arrogance appeared first on Alt-Market.us.

The Recession Of 2025 Will Be Backdated

The Recession Of 2025 Will Be Backdated

Authored by Jeffrey Tucker via The Epoch Times,

It’s a reasonable supposition that a recession will become obvious to all by next summer. It will then be declared by year’s end. The following year it could become backdated with data revisions that take us to 2022. At that point, it will become obvious to people that we have a major problem. Money velocity will freeze up and banks will start failing.

That’s a lot to consider so let’s unpack this a bit.

Consider history. In October 1929, the stock market crashed. Many people on Wall Street suffered but Main Street was largely unaffected. The Hoover Administration got busy with some efforts to loosen credit but without success as credit markets slowly dried up. Throughout 1931, public sentiment toggled between pessimism and denial. Many people thought it was a temporary blip that would go away.

No one called it the Great Depression. That came much later.

By the election of 1932, enough people were concerned about the economic situation but the campaigns did not really focus entirely on that. The big issue was Prohibition. Hoover did not have a strong opinion but Franklin Delano Roosevelt spoke out loudly for repeal. His fiscal policy pushed frugality and balanced budgets, and he decried Hoover as a big spender.

FDR won of course. But before the inauguration, the economic environment became dramatically worse. A banking crisis developed, and FDR used emergency powers to impose a bank holiday and repeal the gold standard. As part of this, he imposed a ban on private gold ownership. It was enforced with fines and jail terms.

Central planning then ensued with massive fiscal stimulus, crazed agricultural policies that required digging up crops to create artificial shortages, and price and wage controls.

All of this unfolded over the course of four years, the first three of which were not at the time thought to be much of a crisis generally speaking. Today it is obvious that 1929 marked the beginning but that was not apparent at the time.

It is not discernible in our time that we are already in recession but that is due to some brittle statistical measures. If you extend the inflation numbers to include housing and interest, plus extra fees and shrinkflation, minus hedonic adjustments, and then adjust the output numbers by the result, you end up in a recession now.

Do you remember the two successive quarters of declining GDP in 2022? At the time, it was said that this was not a recession, even though every definition of recession was two declining quarters of GDP. It was said at the time that the data was not enough to declare it because labor markets were strong.

Trouble was that this too was an illusion. Most of the job gains were in fact in part-time jobs and multiple job holders, and those gains went to foreign-born workers and not natives. Overall, jobs held by native-born workers that are full-time are down relative to four years ago. No one in the mainstream press admitted this.

The jobs report that came out last week was the first glimpse of truth because it was brazenly awful, underperforming every prediction. It also chronicled major job losses in manufacturing and professional services. Those are hard-core recession signs that are likely going to worsen.

All this data will start to be revised next year as the conventional wisdom will change. It will be widely admitted that the economy is weaker than we previously supposed. This will happen regardless of who wins. For one winner, it will serve as an attack and for another winner, it will serve as pretext for extreme intervention like the promised price controls on rents and groceries.

Meanwhile, we will be revisiting the inflation problem. The Fed has already added $1.1 trillion to the money stock over the last 12 months plus lowered interest rates. The effect of this easing has not affected mortgage rates because investors are expecting higher rates in the future. The Fed can control overnight lending but the shape of the yield curve is determined on the bond market.

If major changes are proposed in terms of spending cuts, the bond market will freak out and the United States could repeat the experience of the UK just a few years ago. New prime minister Liz Truss was quickly hounded out of office on grounds that her spending cuts had spooked the bond markets.

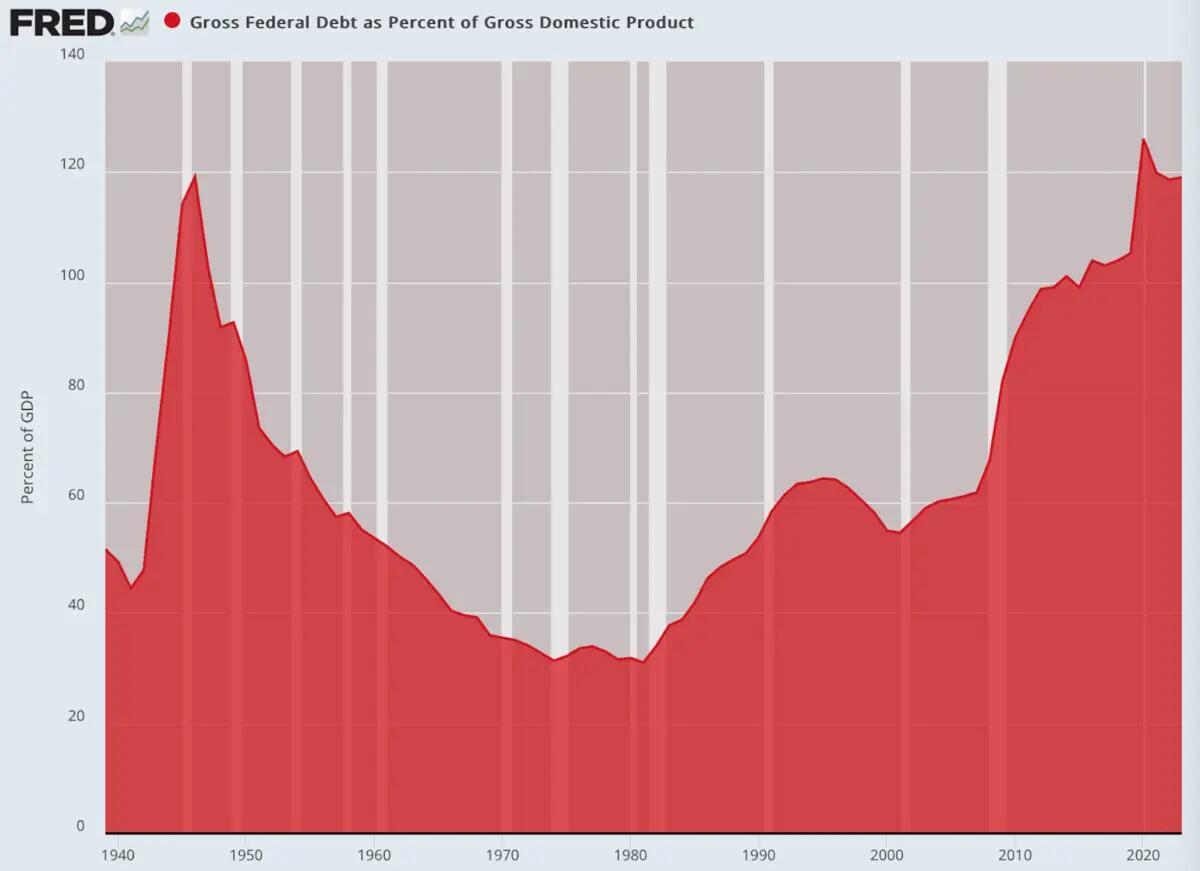

U.S. creditworthiness is already on a hair trigger as the debt pileup has reached astronomical levels. The entire purpose of this wild spending has been to balloon the GDP as much as possible to prevent a recession from being declared already. The debt-to-GDP level is now higher than it was in the Second World War, and getting worse by the day.

(Data: Federal Reserve Economic Data (FRED), St. Louis Fed; Chart: Jeffrey A. Tucker)

The easy solution is dramatic spending cuts but that won’t happen if the bond market starts panicking with quality downgrades. There are only two private institutions that grade U.S. bonds and both are subject to being muscled by political concerns. Such an event could easily overwhelm a new administration. The political people will go into overdrive and demand that the Fed accommodate the bond market, fueling more inflation.

I truly wish that none of this would happen but the truth is that economic forces are always and everywhere more powerful than political ones. There are structural problems alive in U.S. economic life today that are not easily solved by policies of any sort.

But in U.S. political culture, whatever takes place under one president’s watch is blamed on the officeholder regardless. That the circumstances have been created by the previous administration or have nothing to do with existing policy has no relevance in the political culture. That alone makes it nearly impossible for a sitting president to plead with the public for patience.

In 1981, Reagan did make a plea for patience, and lost a great deal of Congressional support in the midterm elections of 1982. He was fortunate that the economic recovery came in time for the 1984 election that granted him a second term. But that was a very close call, and that was also under conditions that were not as structurally dire as conditions today.

As a result, the new administration will encounter pressure to achieve the impossible: immediately improve American living standards without imposing any pain at all. Such a demand is impossible to grant. As a result, whatever happens in this election will likely be reversed in the midterms of 2026, meaning that we cannot count on any kind of policy consistency for many years to come.

Maybe I’m wrong. I hope so. But from what I’m looking at, I don’t see how a frank acknowledgement of current conditions can be put off for another year.

Views expressed in this article are opinions of the author and do not necessarily reflect the views of The Epoch Times or ZeroHedge.

Tyler Durden

Thu, 11/07/2024 – 06:30

3 Tough Questions for the Fed at Thursday’s FOMC Presser

The Fed claims things are going very well, but Fed Chairman Jerome Powell got three questions at the press conference that he had trouble answering honestly.

insiderpaper

- Economics , News , Politics

- November 7, 2024

- 10 views

Vatican hopes for ‘wisdom’ from Trump

The Vatican’s secretary of state congratulated US president-elect Donald Trump Thursday, while expressing doubt that the Republican had a “magic wand” to end conflicts quickly as promised during the campaign. “We wish him a lot of wisdom because that is the main virtue of leaders according to the Bible,” Italian Cardinal Pietro Parolin told reporters […]

The post Vatican hopes for ‘wisdom’ from Trump appeared first on Insider Paper.

German Government Collapses As Mass Strikes Grind Economy To A Halt

German Government Collapses As Mass Strikes Grind Economy To A Halt

It’s not a good day for the establishment. Just hours after Kamala Harris – and the Democrats – staggering loss which ushered in Trump as president for the third time and gave Republicans a sweep of Congress, Germany’s three-party ruling coalition which had been on the verge of collapse for months, imploded on Wednesday evening after Chancellor Olaf Scholz announced he will fire Finance Minister Christian Lindner over persistent rifts on spending and economic reforms, a move that paves the way for a snap election at the end of March.

The firing ejects Lindner’s fiscally conservative Free Democratic Party (FDP) from the troubled coalition, forcing Scholz to call for a confidence vote that he said would take place on January 15. If Scholz loses that vote, which is virtually certain, a snap election is set to take place by March.

The collapse of Germany’s government came just hours after Donald Trump’s clear win in the U.S. election, a result that stunned German political leaders, who depend on American military might for their country’s defense and fear Trump’s tariff policies will hobble German industry.

“Dear fellow citizens, I would have liked to have spared you this difficult decision, especially in times like these, when uncertainty is growing,” said Scholz – viewed as the weakest German chancellor in decades – in a statement at the chancellery.

But the rifts inside the coalition proved too great to overcome. Caught in the middle of an impossible battle, Lindner and his conservative FDP insisted that the German government stick to strict spending rules and cut taxes, even as his left-wing coalition partners wanted to maintain social spending and boost German industry through economic stimulus.

“All too often, Minister Lindner has blocked laws in an inappropriate manner,” said Scholz in a statement. “Too often he has engaged in petty party-political tactics. Too often he has broken my trust.”

Scholz said he had offered Lindner a deal to create an emergency fund to aid Ukraine that would exist outside Germany’s regular budget, but Lindner refused to participate in such fiscal gimmicks that saw the UK recently redefine the nature of “debt.”

“Olaf Scholz has long failed to recognize the need for a new economic awakening in our country,” said Lindner. “He has long played down the economic concerns of our citizens.”

As Politico reports, the FDP is the smallest party in the coalition and is now polling at only four percent — below the threshold needed to make it into the German parliament — meaning its leaders have been mulling a coalition break in order to save their political futures.

Crisis talks in the coalition of Scholz’s Social Democratic Party, the Greens and Lindner’s Free Democratic Party had come to a head after the FDP issued a paper with demands for liberal economic reforms that were difficult for the other two parties to accept.

Lindner’s recent policy paper, leaked to the media last week, called for tax cuts and a scaling back of climate policies in order to stimulate economic growth — both positions that put the party at odds with his coalition partners.

Central to the coalition disagreements was the adoption of the 2025 budget by parliament in which a gap of at least €2.4 billion, and potentially far more, needs to be filled, as well as an agreement on measures to revamp the country’s ailing economy.

The government crisis comes at the worst possible time: Trump’s victory, which anticipates imposing significant tariffs on German exports, is expected to put heavy pressure on Europe’s largest economy. An analysis from the German Economic Institute (IW) estimates that a new trade war could cost Germany €180 billion over Trump’s four years in office.

Many in Germany had hoped that the victory of Donald Trump in the U.S. election earlier in the day would force the coalition to hold together over fears that the incoming president would give Europe’s biggest economy a hard ride, targeting its all-important car industry in a trade war.

Ultimately, however, not even the looming threat of Trump proved enough for the fractious parties to put aside their differences.

Sensing that the economy is about to go from bad to much worse, last Tuesday – amid mounting concern about the imminent collapse of the EU’s largest manufacturing economy – Germany’s giant trade union IG Metall launched strikes in the nation’s metal and electrical industries in an attempt to win higher wages. According to the tabloid Bild, employees began walking off the job during the night shift, including at Volkswagen’s plant in the city of Osnabruck, where workers worry the plant may be closed.

Elsewhere, around 200 employees of the battery manufacturer Clarios went on strike in Hanover, Lower Saxony, carrying torches and union flags, the outlet wrote.

Meanwhile, in Hildesheim, Lower Saxony, around 400 employees, including those at Jensen GmbH, KSM Castings Group, Robert Bosch, Waggonbau Graaff and ZF CV Systems Hannover, have reportedly halted operations.

Protests are also expected at BMW and Audi plants in Bavaria. Work is to be stopped nationwide during the course of the day, the tabloid wrote.

”The fact that production lines are now at a standstill and offices are empty is the responsibility of the employers,” IG Metall’s negotiator and district manager Thorsten Groger stated, as quoted by Deutsche Welle.

IG Metall is demanding a 7% pay raise compared to the 3.6% raise over a period of 27 months offered by employers’ associations, due to soaring inflation. The companies call such demands unrealistic.

The mass strikes come as Volkswagen announced on Monday it would close “at least” three of its ten plants in Germany, lay off tens of thousands of staff and downsize remaining plants in the country. The measures are part of a cost-cutting drive, the conglomerate said earlier. Oliver Blume, chief executive of the VW Group, has cited a “difficult economic environment” and “failing competitiveness of the German economy” as factors behind the decision.

The German Association of the Automotive Industry warned last year that the country was “dramatically losing its international competitiveness” due to soaring energy costs.

A recent survey by the VDA auto industry association suggested that the reshuffling of the German car industry could lead to 186,000 job losses by 2035, roughly a quarter of which have already occurred.

Tyler Durden

Wed, 11/06/2024 – 23:25

Breitbart

- Business , Economics , Entertainment , Gossip , News , Politics , Sports , War

- November 6, 2024

- 9 views

Kamala Harris Campaign Fell $20 Million in Debt in Final Week

Vice President Kamala Harris’s campaign fell $20 million in debt during the final week of her campaign, according to several sources.

The post Kamala Harris Campaign Fell $20 Million in Debt in Final Week appeared first on Breitbart.

- Economics , News , Politics

- November 6, 2024

- 11 views

China’s Xi calls for ‘stable’ US ties in message to Trump

Chinese President Xi Jinping on Thursday called for “stable, healthy and sustainable” ties between Beijing and Washington in a message to US president-elect Donald Trump, state media said. In a “congratulatory message” to Trump, Xi “pointed out that history has shown that China and the United States benefit from cooperation and suffer from confrontation”, state […]

The post China’s Xi calls for ‘stable’ US ties in message to Trump appeared first on Insider Paper.

- Business , Economics , Entertainment , Gossip , News , Politics , Sports , War

- November 6, 2024

- 11 views

Tulsi Gabbard Thanks Trump for Letting Her ‘Play’ a Part in His Campaign

Former Rep. Tulsi Gabbard (R-HI) thanked President-elect and former President Donald Trump for allowing her to “play a small part” in his presidential campaign.

The post Tulsi Gabbard Thanks President-Elect Donald Trump for Allowing Her to ‘Play a Small Part’ in His Campaign appeared first on Breitbart.

{kind=link}

{kind=link}