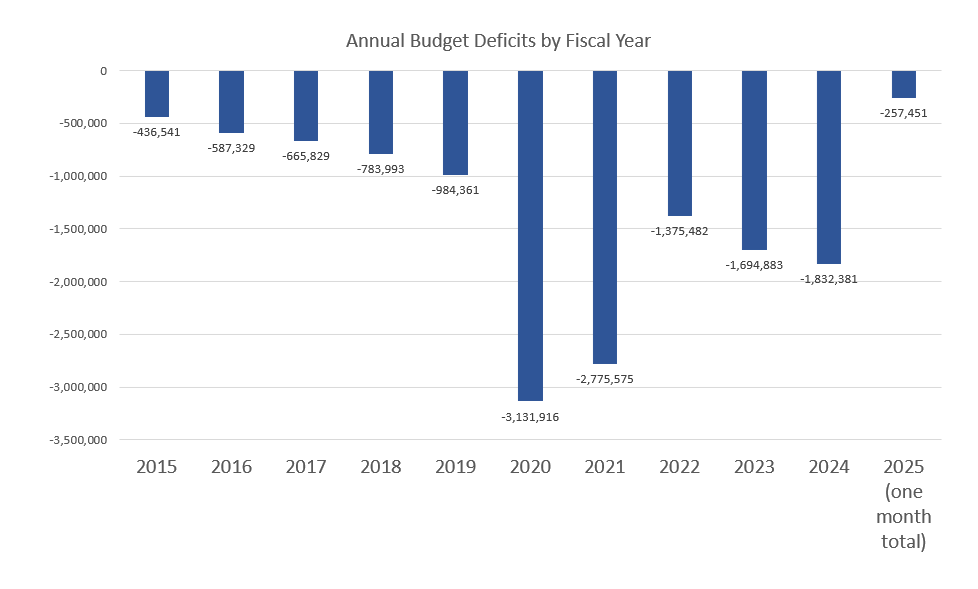

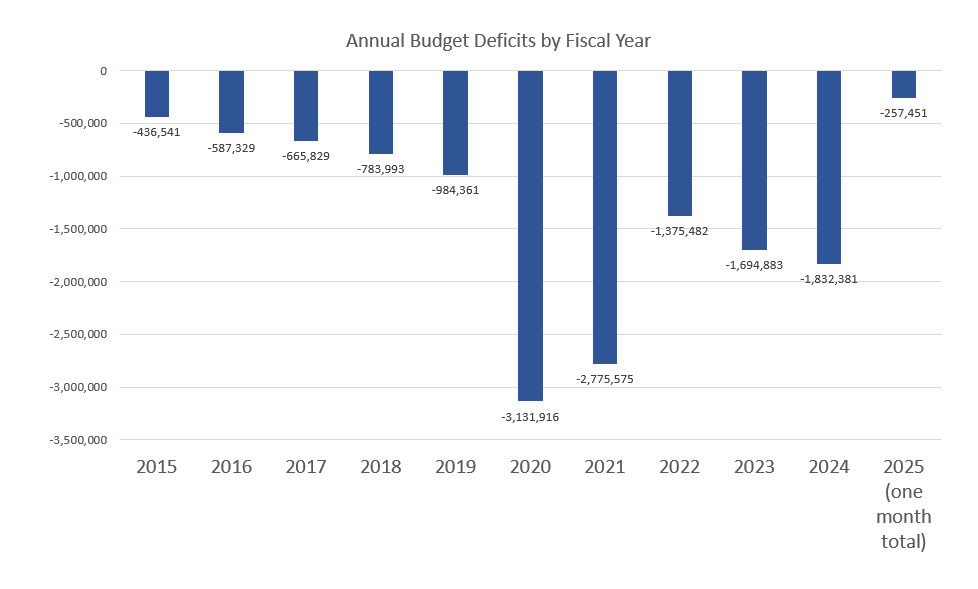

The Treasury Department posted its latest revenue and spending totals this week, and deficits continue to mount at impressive speed. During October—the first month of the 2025 fiscal year—the federal deficit was more than a quarter of a trillion dollars, coming in at $257.4 billion. Tax revenue in October had totaled $326 billion, but spending … Read more

The Treasury Department posted its latest revenue and spending totals this week, and deficits continue to mount at impressive speed. During October—the first month of the 2025 fiscal year—the federal deficit was more than a quarter of a trillion dollars, coming in at $257.4 billion. Tax revenue in October had totaled $326 billion, but spending … Read more

S&P Futures are trading lower this morning in a reaction to comments from Fed Chair Jerome Powell that the Fed is not in a rush to lower rates. Put volumes soar in drug stocks as President-elect Donald Trump nominated Robert F. Kennedy Jr., a vaccine skeptic and critic of federal health agencies, to be his Secretary of Health and Human Services. Two key economic reports due out this morning, Retail Sales and Industrial Production. SEC filings displaying position adjustments at major funds continue to come in, AAPL is seeing an elevated number of firms existing positions in the last quarter. In Europe, stocks have gone from flat two lower as anxiety builds ahead of the U.S. markets open. Oil prices are slightly lower due to global demand concerns.

Peter caps off a very newsworthy week, in which the decisive Trump victory shocked the media class and another Fed rate cut was announced. Peter analyzes both events, arguing against the unbridled economic optimism of Trump’s supporters and criticizing Jerome Powell’s stance on Fed independence and his alarming lack of concern for a future of stagflation.

Peter starts by highlighting the inconvenient trade-off between taxes and government spending. Trump promises new tax cuts, but these will need to be offset by spending cuts, lest the national debt balloons even further out of control:

Trump would have to maybe have a fireside chat in front of the American public and level with them.

He can say, when I was running for president, I promised a lot of things.

I promised a lot of tax cuts… we really need higher taxes if we can’t get some serious cuts in spending.

And so that’s what we’re going to try. I’m going to ask Americans to pitch in and tighten their belts.

While both the Republicans and Democrats like to take credit for for the country’s economic growth, the reality is that much of this “growth” is an artificial boom induced and sustained by decades of expansionary monetary policy by the Federal Reserve:

The problem was we didn’t have a strong economy. We had a bubble. We had a fragile economy.

In fact, we’ve been blowing a bubble in this economy ever since the 1990s. Greenspan is the architect of this house of cards.

He’s been blowing all the air in and every president going back to Clinton has been hiding behind his bubble and has been taking credit for the fake economic growth that has been a consequence of this ever-expanding bubble.

With the stock market lifted by Trump’s success, Peter argues the best time to switch into US equities is when the aforementioned bubble pops. It’ll be painful in the short-term, but that’s when stocks will be a bargain:

The time to load the boat with US stocks is not when they’re historically expensive. I’m waiting for blood in the streets. I want the collapse to happen…

Now, I know when we initially do that and the economy is in recession and everybody is pessimistic, that’s when I’m going to be optimistic, because I’m going to know that this is the bitter tasting medicine that we should have swallowed a long time ago.

Pivoting to the Fed rate cut, Peter points out that the Fed may have cut rates by less than they would have had Kamala Harris been elected instead of Donald Trump:

You would assume that if we’re going to have a stronger economy, the Fed should reconsider the rate cuts, maybe even pause or hike rates.

I thought, well, there’s no chance the Fed’s going to do that. Trump would go ballistic—they’re going to cut. And that’s exactly what they did.

One reason the dollar has been so strong is that people are thinking, well, maybe the Fed won’t cut as much now that we’re expecting a stronger economy.

Peter takes aim at Jerome Powell’s political cowardice, in which he uses the Fed’s independence as an excuse to avoid criticizing bad fiscal policy:

Being independent doesn’t mean you have to keep your mouth shut and you can’t speak your mind and you can’t be critical.

It actually means the opposite of it.

When you’re independent, you’re not influenced by politicians, so you could say whatever the hell you want to say.

You can criticize whoever you want to criticize, and that is exactly what his job is.

At Thursday’s Fed press conference, Powell dodged a question about the possibility of stagflation. Peter sees this as a major gaffe:

He [Powell] kind of says, “Well, our plan for stagflation is to hope there is no stagflation.”

Then he laughed, realizing how ridiculous that sounded.

I mean, what kind of plan is that? Your plan is to hope it doesn’t happen. .. Because obviously, it’s possible.

So, what are you going to do? That’s the question, not what you hope will happen. What’s your plan?

They’ve got no plan. That’s why they hope it doesn’t happen.

But, you know, Murphy has a law, right?

Anything that can go wrong will go wrong. We’re going to have stagflation.

Donald Trump’s has likely halted economic progressivism from corrupting the White House, but with the debt still expanding and the Federal Reserve still setting price controls on interest rates, the economy is far from healthy.

Residents in India’s capital New Delhi again woke under a blanket of choking smog on Friday, a day after authorities closed primary schools and imposed measures aimed at alleviating the annual crisis. Delhi and the surrounding metropolitan area, home to more than 30 million people, consistently tops world rankings for air pollution in winter. The […]

President-elect Donald Trump’s second term in office will likely bring sweeping changes to the nation’s Indo–Pacific policy and ongoing strategic competition with China.

Taiwan’s armed forces hold two days of routine drills to show combat readiness ahead of Lunar New Year holidays at a military base in Kaohsiung, Taiwan, on Jan. 11, 2023. The self-ruled island of Taiwan continues to hold defensive drills, as tensions remain high in the Taiwan Strait. Annabelle Chih/Getty Images

Leaders throughout Congress and the national security space are therefore preparing for an era marked by increased confrontation as the administration pushes back on the Chinese regime’s aggression in the region.

Rep. John Moolenaar (R-Mich.), chair of the House Select Committee on the Strategic Competition Between the United States and the Chinese Communist Party, said he expects a second Trump administration to adopt a firm approach to foreign policy in the Indo–Pacific.

“During Trump’s first administration, peace through strength was at the forefront of American foreign policy,” Moolenaar said in a statement shared with The Epoch Times by the committee’s staff.

That strength, Moolenaar suggests, would extend to the U.S. allies throughout the Indo–Pacific, where Trump is expected to push regional partners to increase their defense spending in order to receive continued U.S. support.

“The entire free world must act with urgency to invest in its collective military power in order to deter conflict, support global prosperity, and defend our values against CCP [Chinese Communist Party] aggression,” Moolenaar said.

Those increased expectations of Washington’s allies could bring both risk and opportunities to U.S. relations in the region as the nation attempts to pressure regional partners into adopting a more forward-facing defense posture.

They will also likely bring increased volatility to the United States’ relationship with China and the CCP, including by shaping the potential for an armed conflict between the two superpowers over the future of Taiwan.

Taiwan Flashpoint

The CCP claims that Taiwan is part of its territory. Though the communist regime has never controlled the island, CCP leader Xi Jinping has made unifying Taiwan with the mainland a legacy issue of his rule and has ordered the Party’s military wing to prepare for a potential conflict by 2027.

The United States does not officially support Taiwanese independence or the forceful unification of the two territories. But, since 1979, Washington has maintained obligations to sell Taiwan the arms it needs to maintain its self-defense.

Likewise, the United States has maintained a policy of so-called strategic ambiguity since 1979, in which it will neither confirm nor deny its willingness to enter a military conflict to defend Taiwan from CCP aggression.

However, U.S. political and military leadership have signaled that they are preparing for such an eventuality. To that end, Chief of Naval Operations Adm. Lisa Franchetti issued a guidance document in September ordering the Navy to prepare for war with China by 2027.

The United States is not interested in preserving Taiwan’s independence simply because of its democratic government. The island nation is responsible for manufacturing more than half of the world’s semiconductors and nearly 90 percent of the globe’s advanced semiconductors, used in electronic components for everything from laptops to pickup trucks to hypersonic missiles.

To that end, Trump’s transactional approach to international security deals has thrown Taiwan’s central role in the global economy into question.

In July, for example, Trump called for Taiwan to pay more for its defense, though the island is already one of the largest purchasers of arms from the United States.

Since 1950, Taiwan has spent more than $50 billion on U.S. weapons, making it the fourth largest purchaser of U.S. arms behind Japan, Israel, and Saudi Arabia, according to the Council on Foreign Relations.

Trump has also suggested that military force would not be necessary to protect Taiwan from the CCP and has instead claimed that a severe enough economic threat to China would prevent an invasion of Taiwan.

Russell Hsiao, executive director of the Global Taiwan Institute think tank, told The Epoch Times that Trump’s ambiguous stance on Taiwan’s defense could invite further CCP attempts to sway American and Taiwanese decision-makers away from aggressively defending the island’s de facto independence.

“The president-elect has already indicated that he would be less clear than President Biden as to whether he thought the United States had an obligation to come to Taiwan’s defense if China decided to invade the island,” Hsiao said.

“Washington and Taipei should be prepared for Beijing to exploit this in its cognitive warfare campaigns and quickly develop their own counter-strategies.”

Hsiao noted, however, that Trump was “unencumbered by past precedents and norms,” which could help him to strengthen the bilateral relationship by overcoming the self-imposed restrictions of the past that have limited U.S. involvement with Taiwan on the international stage.

As such, he said, asking for Taiwan to accept a larger share of the financial burden for its defense could be an opportunity for Taiwanese leaders to demonstrate their resolve and, in the process, garner renewed U.S. support through access to increased arms sales.

“President-elect Trump is expected to emphasize burden-sharing in security ties with allies and partners,” Hsiao said.

“While this may be generally seen in a negative light by most allies and partners, it should be noted that this could lead to it being more forward-leaning in providing a wider variety of arms to Taiwan suited to a range of potential contingencies.”

Trump Expected to Deliver Security—at a Price

Taiwanese leadership responded by saying the island was committed to taking on more responsibility and defending itself from CCP aggression.

Taiwanese leadership may consider making a substantial arms purchase early on in the second Trump administration as a sort of down payment to demonstrate its resolve to the administration.

John Mills, former cybersecurity chief in the Office of the Secretary of Defense, said that ensuring a robust defense budget would help Taiwan to make sure U.S. support did not flag and that military expenditure was “the primary metric” used by Trump to determine an ally’s willingness to defend itself.

“We have a very poor track record when we carry the burden for other countries,” Mills said.

“All that is being asked is at least 2 percent of GDP spent on defense and, in reality, 4 to 5 percent is the new 2 percent.”

At present, Taiwan spends about 2.4 percent of its GDP on defense, according to data compiled by the CIA.

Other U.S. allies in the region are more varied. South Korea spends about 2.7 percent of its GDP on defense, and the Philippines spends only about 1.5 percent. Japan is in a unique situation because it is currently spending 1.4 percent but is in the middle of a historic reform of its military policy and strategy, which will see that figure rise to at least 2 percent in the coming years.

Yet none of those numbers at their current levels are likely to please the incoming Trump administration if it is truly so set on encouraging the nation’s allies in the Indo–Pacific to take point on confronting the Chinese regime’s global expansion.

There may be some wiggle room, however, as the administration looks to use less traditional pathways to secure its international interests.

Sam Kessler, a geopolitical analyst at the North Star Support Group risk advisory company, said that a hallmark of the first Trump administration was its ability to think outside of the box, and that would likely only increase now, given Trump’s growing distance from the old guard of the Republican Party.

“The Trump administration in the first term was innovative, proactive, and resourceful in the deals and agreements they crafted, so expect something similar, as well as a little predicted unpredictability, too,” Kessler told The Epoch Times.

“This may be done in the form of trade deals, security arrangements, foreign investments, and policies that may help reduce the threat levels, too. It could be a wide range of things that could be utilized.”

On that note, Kessler suggests that Trump would revisit trade deals and strong economic measures when confronting China and might prove surprisingly willing to take a proactive stance in the bilateral relationship with China.

Such economic deals, he said, could have the secondary objective of smoothing out regional tensions and preserving allied security while holding the CCP accountable economically.

“We may end up witnessing a series of deals and agreements that may be related to multiple issues that are non-related to the original purpose of a negotiation in order to reduce tensions between multiple parties in other areas,” Kessler said.

In all, it is clear that U.S. allies in the Indo–Pacific will be expected to contribute more to the common defense in the region, and such efforts will not go unseen.

With that much in mind, Mills said that he believes the likelihood of an armed conflict would drop, as Trump’s expectations for all nations in the Indo–Pacific would be clear.

“The likelihood of conflict in the western Pacific decreases significantly under Trump,” Mills said.

“Why? Because he’s showing clarity and resolve at all times. Clarity and resolve help prevent war. Lack of clarity and resolve creates war.”

“The left sees how effective and how impactful he’s been, and he’s got Trump’s ear helping make some of the most historic decisions for these Cabinet picks.”

Former President and President-elect Donald Trump made inroads across several demographics, including young voters, and some are revealing why they opted to cast their ballot for Trump over Vice President Kamala Harris and her running mate, Minnesota Gov. Tim Walz.

{kind=link}